Novo vs Bluevine: Banking with no guesswork

See how Novo and Bluevine compare across interest and rewards, integrations, invoicing, and funding, so you can choose the right fit for your business.

How novo compares to Bluevine

Less tools, more money in

"I was using personal accounts, sending invoices in Google Docs, and getting paid through PayPal. It felt messy and unprofessional. Now I have a dedicated account, seamless invoicing, and I just download my reports come tax season."

Features

Bluevine

Monthly fees

$0

$0-$95

Integrations

QuickBooks; limited ecommerce integrations

Built-in Invoicing

Automated Budget Allocation

Faster Payments

Automatic Expense Categorization

Integrated bookkeeping via partner apps/tools

2% Cashback Business Credit Card

ATM Access & Fees

$7/month ATM fee reimbursement

Fee-free in-network; fees out-of-network

High-Yield APY

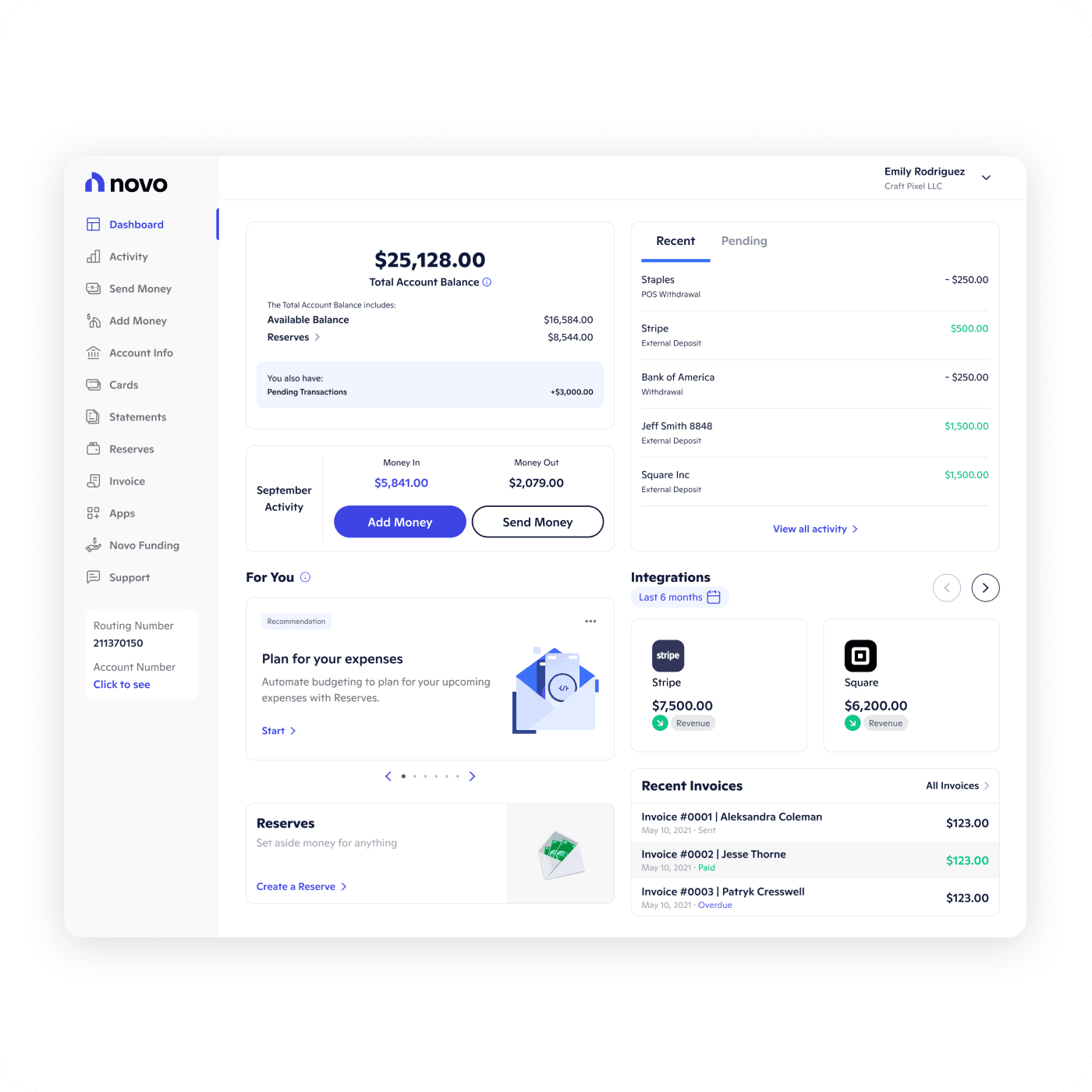

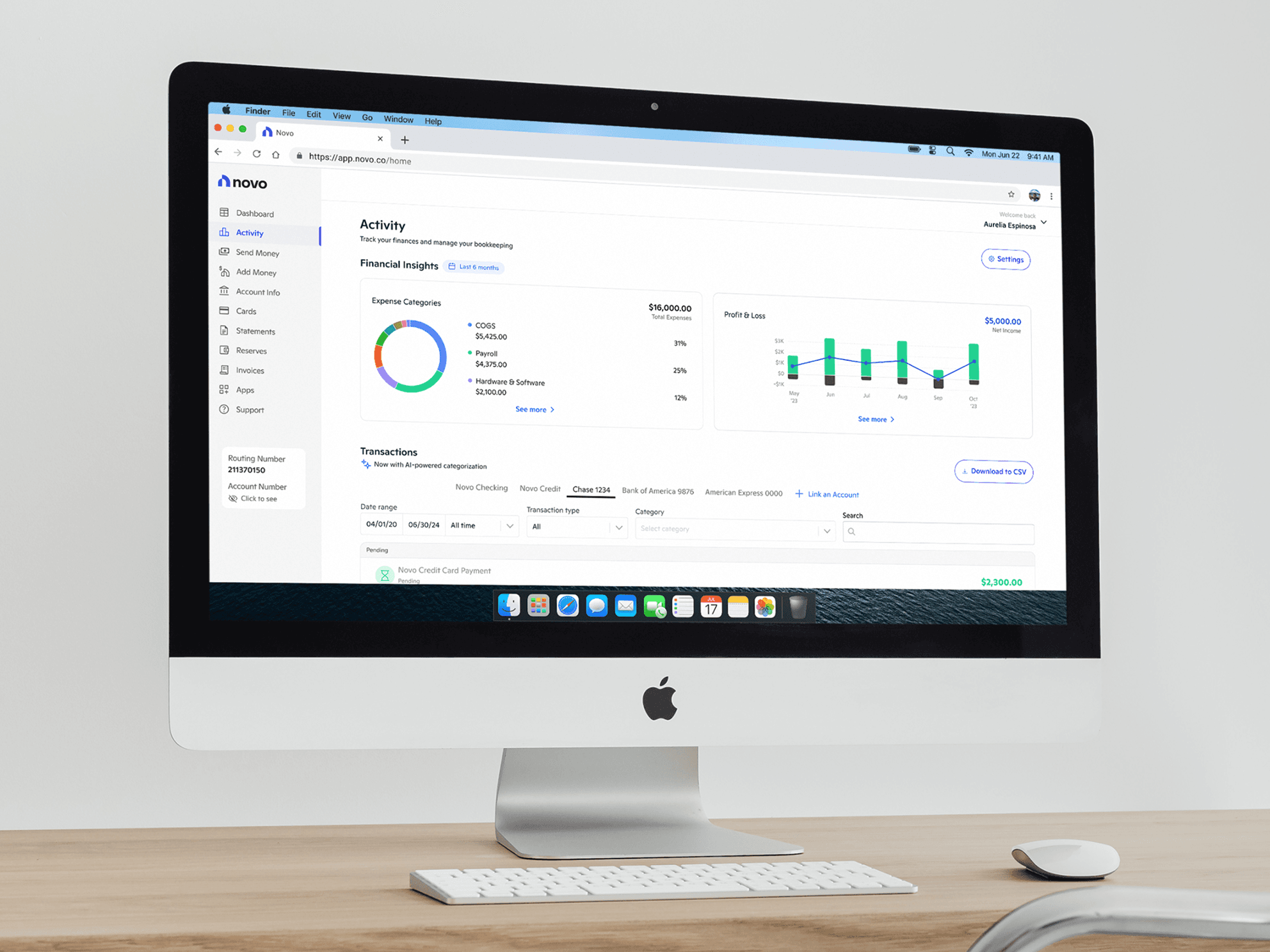

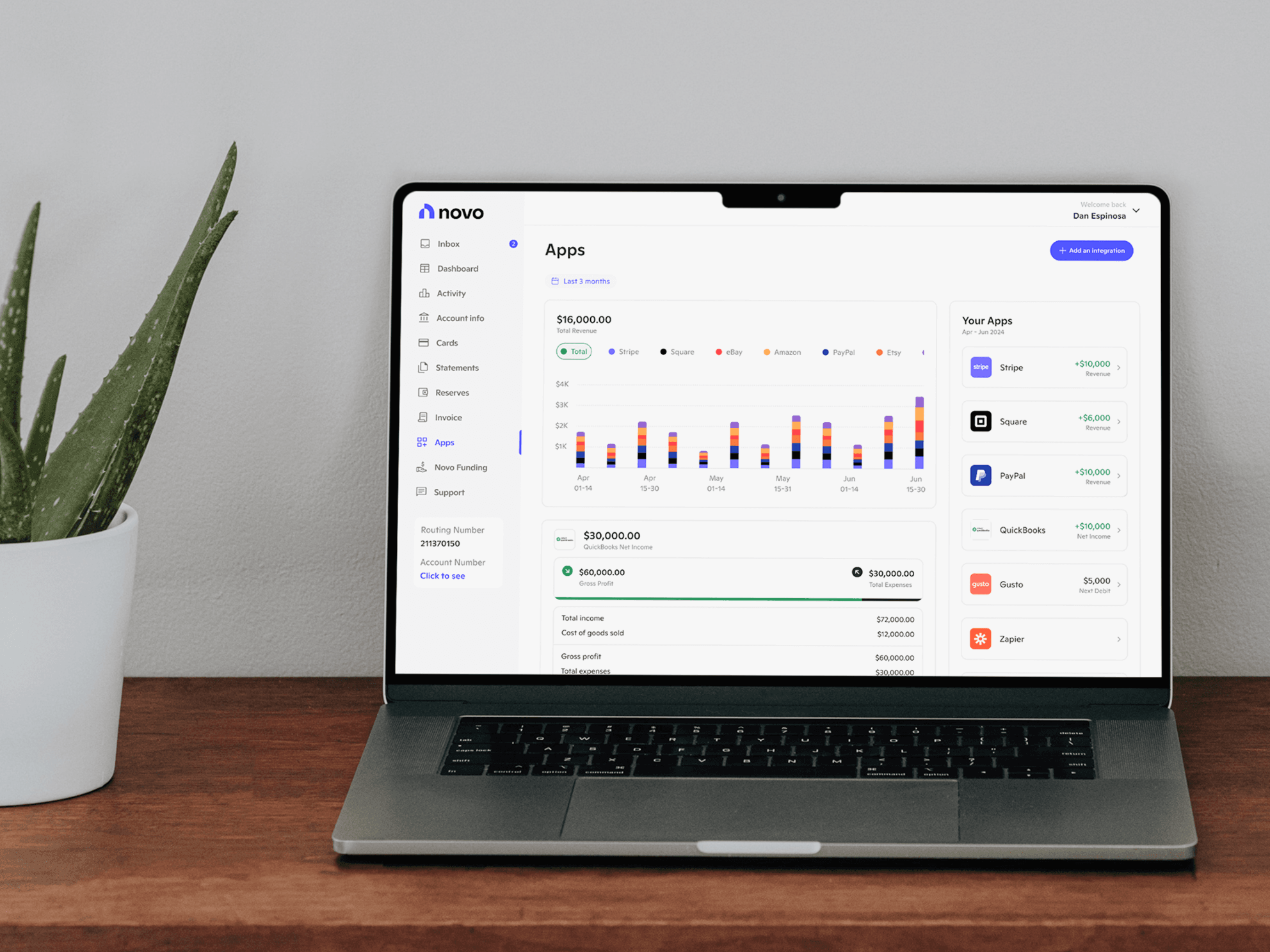

HOW TO PUT NOVO TO WORK

Our all-in-one dashboard lets you see what's coming in, what's going out, and what needs your attention without digging through spreadsheets.

What other independent business owners are saying

No delays, no friction, no headaches

Novo has completely simplified how I manage my business finances. I can track cash flow in real time, organize expenses, and move money fast. No delays, no friction. It keeps me focused on clients instead of fighting with outdated banking.

Frequently asked questions

Yes, Novo offers a business credit card with 2% cashback, giving you rewards on everyday business spending. Bluevine does not offer a business credit card.

Novo offers Express ACH for eligible customers, helping you access funds faster than standard ACH timelines.

Novo offers direct integrations built specifically for e-commerce and service-based businesses.

Novo offers Funding for eligible customers designed for flexible access to working capital.